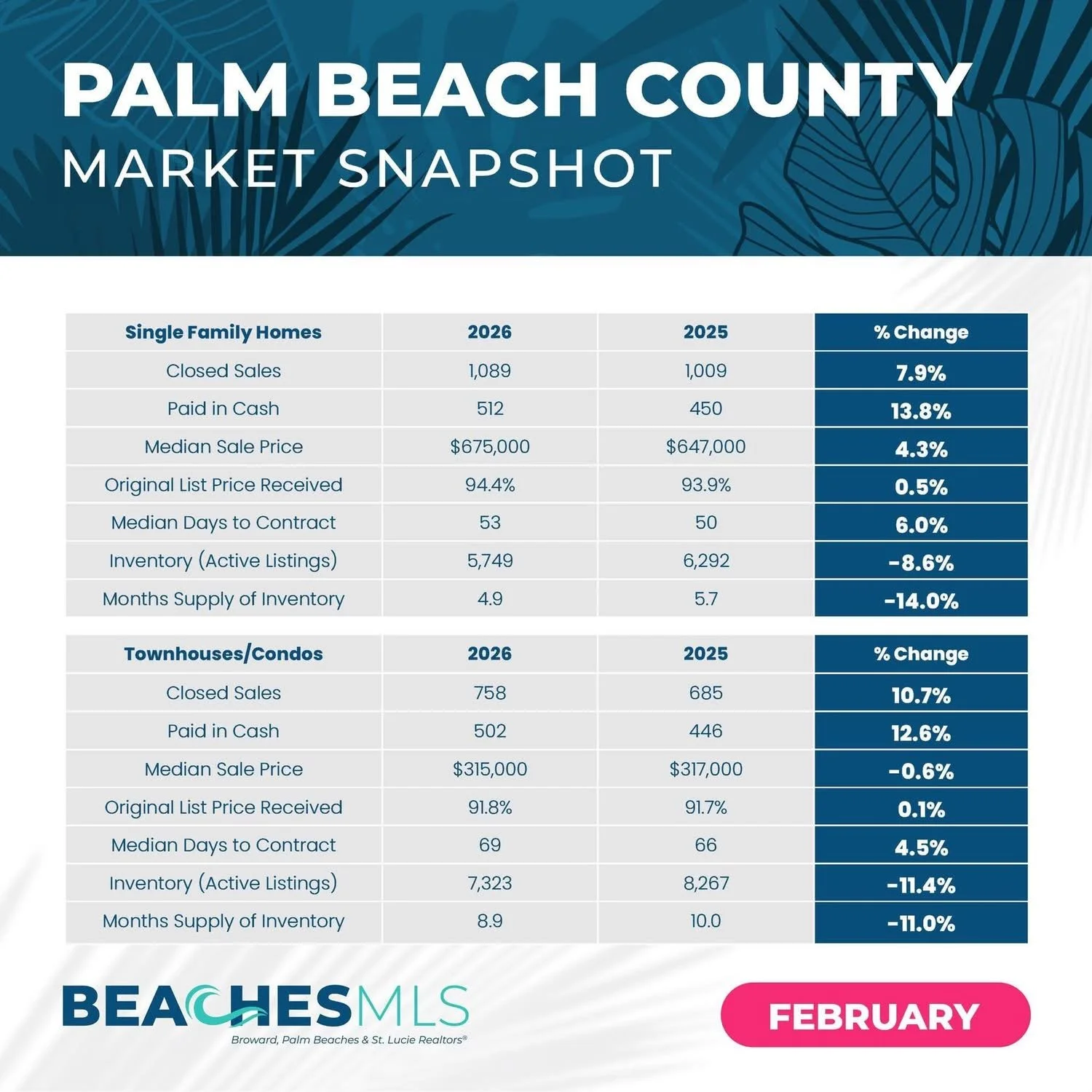

The Palm Beach County housing market continues to show resilience and positive momentum as we progress through early 2026. According to the latest data from BeachesMLS (covering Broward, Palm Beaches, and St. Lucie Realtors®), February brought notable year-over-year gains in sales volume, steady price appreciation in single-family homes, and a tightening inventory that points to a competitive environment, especially for single-family properties. Here's a clear breakdown of the key trends for both single-family homes and condos.

Single-Family Homes: Strong Demand and Price Growth

The single-family segment performed particularly well in February 2026 compared to the same month in 2025:

Closed Sales: 1,089 (up 7.9% from 1,009)

Cash Purchases: 512 (up 13.8% from 450): Highlighting the continued strength of cash buyers in the market

Median Sale Price: $675,000 (up 4.3% from $647,000): Reflecting solid appreciation without signs of overheating

Original List Price Received: 94.4% (slight improvement from 93.9%)

Median Days to Contract: 53 days (up 6.0% from 50 days), indicating homes are still moving relatively quickly

Active Inventory: 5,749 listings (down 8.6% from 6,292)

Months Supply of Inventory: 4.9 months (down 14.0% from 5.7 months): This level suggests a seller-leaning to balanced market for single-family homes, with less supply putting upward pressure on prices

Overall, single-family homes saw higher transaction volume, more all-cash deals, and reduced inventory, creating a tighter and more favorable environment for sellers.

Townhouses and Condos: Increased Activity with Slight Price Softness

The condo and townhouse market showed even stronger sales growth, though median prices dipped modestly:

Closed Sales: 758 (up 10.7% from 685)

Cash Purchases: 502 (up 12.6% from 446)

Median Sale Price: $315,000 (down 0.6% from $317,000)

Original List Price Received: 91.8% (minor uptick from 91.7%)

Median Days to Contract: 69 days (up 4.5% from 66 days)

Active Inventory: 7,323 listings (down 11.4% from 8,267)

Months Supply of Inventory: 8.9 months (down 11.0% from 10.0 months)

While prices softened slightly (possibly due to more options for buyers in this segment), the notable increase in closed sales and cash transactions, combined with declining inventory, indicates improving buyer interest and momentum heading into spring.

What This Means for Buyers and Sellers

Palm Beach County's market remains healthy and dynamic. Single-family homes are in especially short supply, which supports continued price growth and faster sales for well-priced properties. Condos and townhouses offer relatively more inventory (still trending downward), giving buyers a bit more negotiating room in that category.

Cash buyers continue to play a major role representing nearly half of single-family transactions and a similar share in condos, which underscores the appeal of the area for investors and relocators seeking stability.

As we approach the traditionally busier spring season, expect competition to heat up further, particularly for single-family homes. If you're considering buying or selling in Palm Beach County (including areas like my hometown of West Palm Beach), now is a great time to consult local data and a trusted realtor to navigate these trends.

Data source: BeachesMLS: Broward, Palm Beaches & St. Lucie Realtors® (February 2026 report). Markets can shift quickly, so stay informed with the latest reports.